In Lobster & Co Trading Pty Ltd v Nisbets Australia Pty Limited [2023] NSWSC 1179 (29 September 2023) the Supreme Court had to decide if there was an agreement for chairs to be delivered by a specific date.

The facts

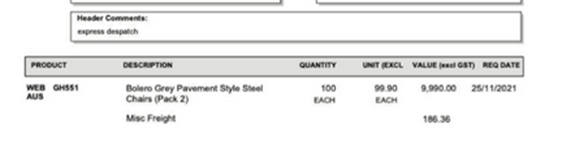

On or about 24 November 2021 the plaintiff and defendant entered into an agreement whereby the defendant agreed to supply the plaintiff with 100 (one hundred) Bolero Grey Pavement Style Steel Chairs (Steel Chairs) in consideration for payment of $11,194.00 (the Agreement).

The plaintiff argued that it was a term of the Agreement that the defendant deliver to the plaintiff the steel chairs by 22 December 2021 (Delivery Date), and that in breach of the Agreement, the defendant failed to supply the steel chairs to the plaintiff by the Delivery Date.

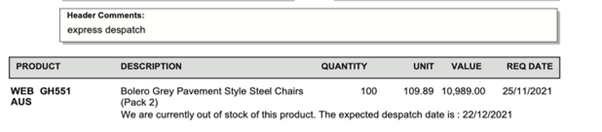

The contract for sale comprised two documents: a pro-forma tax invoice and a sales acknowledgement receipt.

Part of the pro forma tax invoice is copied below:

Part of the sales acknowledgement document is copied below:

The sales acknowledgement document states under header comments “express dispatch” and at the bottom of the form it states “we are currently out of stock of this product. The expected dispatch date is 22 December 2021.

The plaintiff argued that the defendant had represented that the chairs would be delivered by 22 December 2021. The magistrate in the Local Court was not satisfied that the defendant’s notation on the sales acknowledgment document “The expected despatch date is: 22/12/2021″ was a representation that the chairs would be delivered by 22 December 2021. The magistrate interpreted those words to mean “We hope to be able to despatch these chairs on 22 December” and therefore there was no promise that the chairs would be delivered by that date. This is in the context of the Local Court’s finding that the chairs were delivered on 3 February 2022.

The plaintiff appealed the magistrate’s decision.

The appeal judge found that:

This document [the sales acknowledgement document] stated expected dispatch date, not delivery date, i.e. likely dispatch from China. The Sales Acknowledgement also used the phrase “expected dispatch date” – on any view, this is far from guaranteed.

The Magistrate found, after asking herself “what do these words mean?”, that “it is clear that the defendant company did not have these chairs within its control at this date. It was reliant on someone else or some other way of obtaining these chairs…In my view, the words mean, ‘We hope to be able to dispatch these chairs on 22 December”.

In my review, this reasoning discloses no error.

Lesson

- The defendant in this case should have required wording similar to this:

The chairs must be delivered to the defendant’s address by no later than 22 December 2021,

To be included in both the tax invoice and sales acknowledgement document under the heading Header Comments. - Alternatively, the defendant could have emailed the plaintiff on paying the tax invoice wording similar to this:

This payment is contingent on the chairs being delivered to the defendant’s address by no later than 22 December 21.

If you have any questions, please contact us.